(Bloomberg) — For years, buyout firms used controversial loans backed by their equity stakes to juice up returns in their funds. After attracting criticism from some of the same investors the practice was supposed to benefit, they are hitting the brakes.

Most Read from Bloomberg

Net-asset-value loans, which layer extra leverage onto private companies already carrying heavy debt, have come under scrutiny, especially when buyout firms use them to fund distributions rather than growth. Many firms borrowed against their portfolio companies to keep the private market bonanza alive while deal-making withered.

With even investors on the receiving end of those payouts flagging concern, there are moves afoot to shift how NAV loans are being spent. Ares Management Corp., Perpetual Investors and 17Capital all say NAV loans are increasingly being reinvested into portfolio companies or used to make add-on acquisitions, rather than fund payouts.

In part, it points to a shift in the balance of power that’s allowing investors in private equity funds such as pension funds, known as limited partners or LPs, to hold sway over private equity managers known as general partners or GPs.

“Using NAV loans for distributions is somewhat like kicking the can down the road,” said Christian Wiehenkamp, chief investment officer of Perpetual Investors. “LPs don’t seem to like that and since GPs are no longer calling the shots without respecting the nature of a longer partnership, GPs seem to have listened.”

While NAV loans have existed for more than a decade, they became a crutch for PE firms during a recent deal drought, helping to drum up cash they’d normally have found from asset sales. Now totaling about $50 billion, according to estimates from Ares, NAV loans have elicited warnings from regulators concerned their risks could spread through the financial system.

There’s a risk that the loans weaken portfolio companies, and that, even if they puff up returns at first, they dilute them in the long run.

“I’m sure there are some LPs who would have loved to get distributions through any means they could over the past couple of years,” said David Wilson, a partner at 17Capital, a leading provider of NAV loans. “Other investors who are sitting on a lot of cash may see this as an expensive way to get cash back.”

Data on the use of NAV loans is patchy at best. How private equity finances itself and where it raises its money is one of the most closely guarded secrets of this already opaque sector. But the trend suggests firms are forgoing some of the deals that are raising alarms.

“Money-out” transactions, where the sole use of proceeds is to make a distribution to limited partners for liquidity or performance purposes, accounted for only 3% of 2023 volume, according to research from 17Capital that includes deals done by some competitors. That’s down from 24% in 2022.

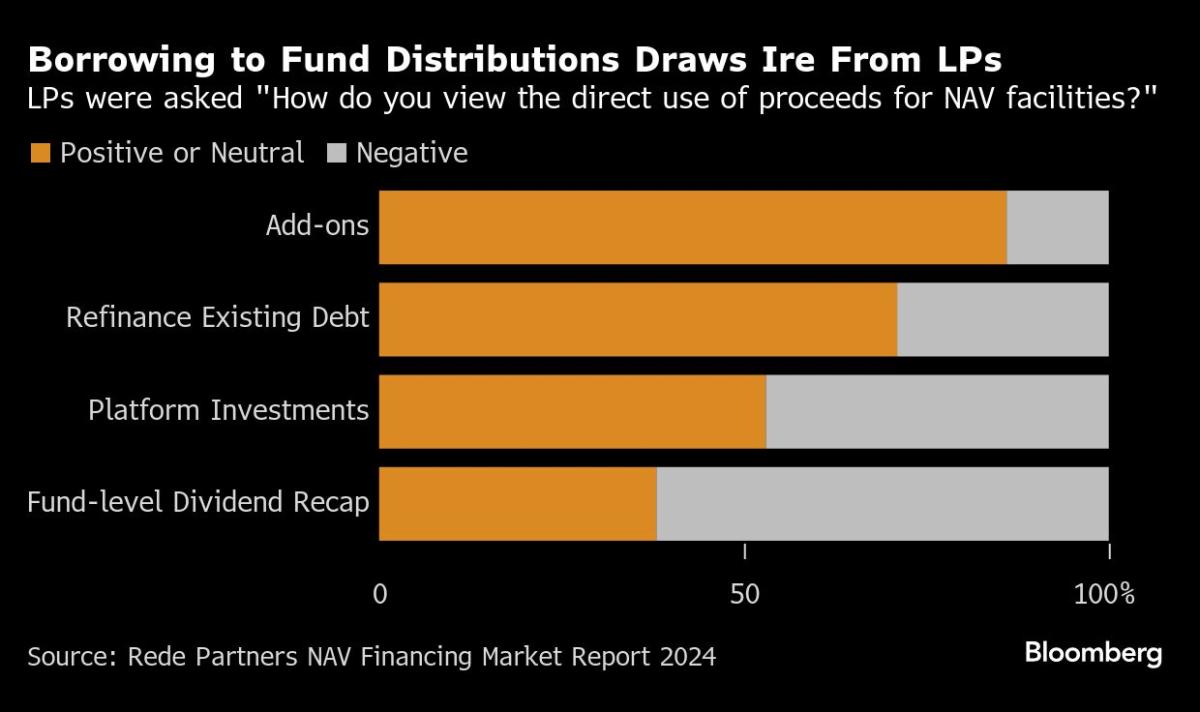

17Capital’s own pipeline suggests that figure is 2% for 2024, though the firm said data for the period is still incomplete. Investors in private equity are overwhelmingly in favor of reinvesting cash raised from NAV loans, according to a survey by Rede Partners.

“It’s a trend that we’ve seen LPs support,” said Richard Sehayek, managing director in alternative credit at Ares. “Now there’s much more discussion with investors, more transparency and more education.”

Bryan Barreras, counsel for Cadwalader, Wickersham & Taft who represents NAV lenders, contends the debt is less risky than many people think because loans are backed by collateral usually three times more than their value.

Still, the Institutional Limited Partners Association, a trade body for investors to PE firms, has argued that private equity firms should alert investors before they borrow against their funds’ assets. The risk is that any distributions they receive from a NAV-based facility could later be recalled to help pay down the loan, according to the ILPA.

“The ILPA guidance focused quite a bit on the money-out transactions, even though it’s such a small part of what’s happening out there,” said Wilson at 17Capital. “The guidance was about making sure that NAV loans are being used properly rather than saying they shouldn’t be used at all.”

Deals

Banco BPM SpA is seeking investors for two significant risk transfers linked to loan portfolios worth about €4.5 billion

Direct lenders including Antares Capital, Blue Owl Capital Inc. and KKR & Co are preparing to take over insurance claims manager Alacrity Solutions, the latest restructuring in the private credit market

KKR & Co. is providing about £1.3 billion of debt for Constellation Automotive Group, the used car marketplace owned by TDR Capital

Biotechnology company Thermo Fisher Scientific has signed a deal to borrow 1.15 billion Swiss francs through a privately placed bond sale

Private credit firm Golub Capital has completed its $200 million equity investment in Nassau Financial Group, becoming the insurance specialist’s largest minority holder

CVC Cordatus Opportunity Loan Fund is planning a potential refinancing, and sent a notice of intention to shareholders

Carlyle’s global credit platform has provided Scandinavian company Jordanes with a NOK2.75 billion ($250 million) financing package

Fundraising

Job Moves

Apollo Global Management Inc.’s head of private equity capital markets, Matthew Manin, has left the firm to pursue another opportunity

Point72 Asset Management hired Todd Hirsch, a former Blackstone Inc. senior managing director, as head of private capital

Blackstone Inc. is hiring a pair of credit veterans, Andie Goh and Jack Ervasti, to cover investment-grade deals as the world’s largest alternative-asset manager continues its expansion into private credit

Did You Miss?

After Year of Pressure, Private Credit Eyes a Way Out: Analysis

Private Credit Downgrades to Stabilize in 2025, Fitch Says

Big Questions Behind the Push for Alternatives: Wall Street Beat

India Stocks Decline, Weighed by Private Lenders HDFC and ICICI

Private Credit Defaults May Reach 3% in Consumer Sector: KBRA

–With assistance from Rene Ismail and Isabella Farr.

All three projects have secured tax equity partnerships and power purchase agreements. Credit: Ørsted. Ørsted has divested a 50% equity stake in three US onshore […]

Despite high borrowing costs and extended hold times in 2024, dealmaking roared ahead for healthcare private equity with a heavy focus on biopharma North American […]

Interactive Strength Inc. TRNR shares are surging premarket on Thursday after the company inked a non-binding letter of intent and exclusivity agreement to acquire a […]